The Billionaire Class

There are 800 or so of them in the United States alone. Where the hell did they come from?

Discussing Steven Taylor’s post yesterday that concluded, “I fear that we are seeing a significant shift toward direct oligarchic power in our elections which is not healthy in the least,” regular commenter @Beth observed,

I think Billionaires are a whole class of rich that is new, different, and way more destabilizing. I don’t have time now, but it would be interesting to compare say the Gilded Age Rich vs the Billionaires now. Or even just the growth of Billionaires in the U.S. I suspect that prior to about 1990 the number of Billionaires could be counted on 2 hands max. Now we have dozens if not hundreds of them and they can effect things more than the ordinary rich can because the difference between say having 100 million and having 1 billion is HUGE. Most people don’t understand how huge.

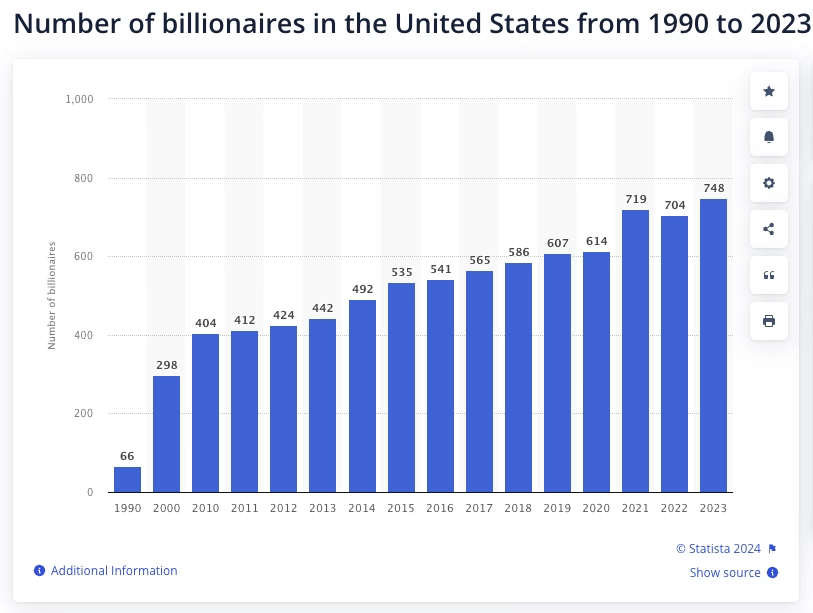

I remember being fascinated by the Book of Lists as a kid and at that time (the first edition came out in 1977), there were something like four or five billionaires on the planet. There are now so many of them in the United States alone that we can’t count all of them. The folks at Statista provide this handy dandy chart:

Certainly there has been considerable inflation of the 34 years covered–$1000 in 1990 has the same buying power as $2476 today—but that only gets us to 164. Ditto population growth—we only had 250 million people in 1990 and are up to 335 million now. But, again, that only accounts for a fraction of the growth. My guess is that the dot com boom of the 1990s created that initial spike; most of the growth since then looks much more natural.

A NYT Magazine feature from April 2022 titled “How Many Billionaires Are There, Anyway?” gets at the question. It starts with Malcolm Forbes’ idea in 1981 to create a now-famous list.

The resulting reporting project took a year, dozens of flights and thousands of interviews. At the top of the very first Forbes 400 list was Daniel K. Ludwig, a shipping magnate, estimated by the magazine to be worth more than $2 billion.

If you simply adjusted for inflation, that’s now at least $5.8 billion, a fortune that would land Ludwig in a seven-way tie for the 182nd spot on the last Forbes 400 list, alongside Fred Smith, the founder of FedEx; Gary Rollins, chief executive of Rollins, Inc., which owns several pest-control companies; and who could forget Peter Gassner, the head of a cloud-software company called Veeva. Fortunes at this tier hardly seem to merit media coverage anymore.

Indeed, one of the things that always surprises me about these lists is how anonymous most of the members are. Elon Musk, the current World’s Richest Man and the subject of Steven’s observation, is rightly a household name. For that matter, most have heard of Fred Smith and everyone has heard of FedEx. But neither Rollins nor Veeva ring a bell with me.

How can someone amass that kind of money in an enterprise that doesn’t even register with the public? I’m reminded of an old Chris Rock joke:*

In my neighborhood, there are four Black people. Hundreds of houses, four Black people. Who are these Black people? Well, there’s me, Mary J. Blige, Jay-Z and Eddie Murphy. Only Black people in the whole neighborhood. So let’s break it down, let’s break it down: me, I’m a decent comedian. I’m a’ight. Mary J. Blige, one of the greatest R&B singers to ever walk the Earth. Jay-Z, one of the greatest rappers to ever live. Eddie Murphy, one of the funniest actors to ever, ever do it. Do you know what the White man who lives next door to me does for a living? He’s a f**king dentist! He ain’t the best dentist in the world…he ain’t going to the Dental Hall of Fame…he don’t get plaques for getting rid of plaque. He’s just a yank-your-tooth-out dentist. See, the Black man gotta fly to get to somethin’ the White man can walk to!

But I digress.

Almost everyone at the top of the list is easily recognizable for what they or an ancester did:

The process has become easier in one sense, because our access to information is so much better; and harder, because there are so many more billionaires. The 2022 World’s Billionaires list, for example, grew by 573 names compared with the last prepandemic list, in 2020. That year, the world was minting new billionaires at a rate, Forbes noted, of about one every 17 hours. At the top of the new list is Elon Musk, with an estimated net worth of $219 billion; behind him is Jeff Bezos, with $171 billion. From there, it goes like this: Bernard Arnault and family ($158 billion), Bill Gates ($129 billion), Warren Buffett ($118 billion), Larry Page ($111 billion), Sergey Brin ($107 billion), Larry Ellison ($106 billion), Steve Ballmer ($91.4 billion) and Mukesh Ambani ($90.7 billion), the richest man in Asia and, I confess, the highest-ranked person on the list I’d never heard of.

Not only are those numbers staggering but they’re volatile. Two years later, Musk’s wealth has reportedly almost doubled. He’ll make more money as I’m typing this sentence than I’ll make in my whole life—and I’m doing pretty well.

If you continue down, keeping your eyes on the Americans, most are familiar, names you know from the vast fortunes cast off by Silicon Valley, or Walmart (the wealthiest Walton heirs have around $65 billion each), or Nike ($47.3 billion), or divorcing Jeff Bezos ($43.6 billion), or living longer than Sheldon Adelson ($27.5 billion). But eventually, you start to encounter less-familiar names: Thomas Peterffy, who immigrated from communist Hungary and pioneered computerized stock trading (No. 80, $20.1 billion); Robert Pera, who founded something called Ubiquiti Networks and — this was fun to learn — went to the same state college that I did (No. 127, $14.6 billion); speaking of college, there’s Dustin Moskovitz, who was roommates at Harvard with another guy who had a cool idea for a social network (No. 167, $11.5 billion). Before long, you’re down with the Peter Gassners of the world, and there are a lot of them — America has some 735 billionaires now according to Forbes, collectively worth more than $4.7 trillion. A decade ago, Forbes counted only (“only”) 424. A decade before that, 243. They keep multiplying, and their collective wealth grows, even, or especially, as the rest of us fall behind.

Editorializing aside, the question is How? If someone earned $100 million a year—which is a lot!—it would take ten years to earn a billion and four thousand years to get to Musk’s number. And few people, indeed, can sustain that kind of income over four thousand years.

The NYT billionaires feature spends several paragraphs ranting about policy changes initiated during the Reagan administration, notably a huge cut in the top marginalized tax rate and the Fed’s prioritization of reining in inflation. While both doubtless help explain the accumulation of wealth in the United States, the fact that the explosion of the billionaire class is a global phenomenon suggests that Republican policies are not the chief explanation.

Regardless, this makes sense:

In his book “Ages of American Capitalism,” the University of Chicago historian Jonathan Levy describes the era of capitalism we live in as the Age of Chaos: a time in which capital has become more footloose, liquid and volatile, constantly flowing into and out of booms and busts, in contrast to the staid order — and widely shared prosperity — that characterized the industrial postwar economy.

[…]

This shift to a highly financialized, postindustrial economy was helped along by the Reagan administration, which deregulated banking, cut the top income tax rate to 28 percent from 70 percent and took aim at organized labor — a political scapegoat for the sluggish, inflationary economy of the ’70s. Computer technology and the rise of the developing world would amplify and accelerate all these trends, turning the United States into a sort of frontal cortex for the globalizing economy. Just as important, the tech revolution created new ways for entrepreneurs to amass enormous fortunes: Software is by no means cheap to develop, but it requires fewer workers and less fixed investment, and can be reproduced and shipped around the world instantaneously and at practically no cost. Consider that the powerhouse of 20th-century capitalism, Ford Motors, now employs about 183,000 people and has a market capitalization close to $68 billion; Google employs about 156,000 people and has a market cap of around $1.8 trillion. This new economy would be run by, and for, knowledge workers, who would reap most of the gains, and therefore have more money to spend on services — a sector that would come to sort of, but never fully, replace the manufacturing this transformation did away with.

“During the Reagan years,” Levy writes, “something new and distinctive emerged that has persisted down to this day: a capitalism dominated by asset price appreciation.” That is, an economy in which the rising price of assets — stocks, bonds, real estate — would be, somewhat counterintuitively, a fuel for economic growth. It has been a good time, in other words, to own a lot of assets. And owning assets is mostly what billionaires do.

Whether a direct result of government policy or merely helped along by it, we simply have a radically different economic system. This isn’t new news, of course, but it does lead to the concentration of wealth.

In his book “Capital in the Twenty-First Century,” the French economist Thomas Piketty notes that the new economic order has made it difficult for the superrich not to get richer: “Past a certain threshold,” he writes, “all large fortunes, whether inherited or entrepreneurial in origin, grow at extremely high rates, regardless of whether the owner of the fortune works or not.” He uses the examples of Bill Gates and Liliane Bettencourt, the heiress to the L’Oréal fortune. Bettencourt “never worked a day in her life,” Piketty writes, but her fortune and Gates’s each grew by an annual rate of about 13 percent from 1990 to 2010. “Once a fortune is established, the capital grows according to a dynamic of its own,” Piketty notes, adding that bigger fortunes tend to grow faster — no matter how extravagant, their owners’ living expenses are still such a small proportion of the returns that even more is left over for reinvestment.

This isn’t shocking, of course. The Gates-Bettencourt illustration is a useful one. During all but the last two years of the period in question, Gates was the CEO of Microsoft. In that capacity, he generated a vast amount of wealth for the economy at large and has share of it, mostly in the form of Microsoft stock, while tiny as a percentage, was nonetheless enormous. An heiress, meanwhile, would earn the same return simply buying a ton of Microsoft stock in 1990 and holding on to it. In both cases, their wealth came from their money working, not their own labor.

Piketty was writing in 2013, while the economy was still recovering from the financial crisis of 2008. That recovery was buoyed by several years of near-zero interest rates, kept there by the Fed on the theory that, with credit widely available, the economy would regain its health. But low interest rates do two things: They push investors into riskier territory seeking better returns (and ideally creating jobs in the process); and they inflate the value of assets. Private equity and venture capital benefited greatly from this low-rate environment, helping both Silicon Valley and the financial engineers of Wall Street clean up once more. Even in less-dynamic sectors of the economy, the cheap money enabled an explosion in stock buybacks, some $6.3 trillion worth during the 2010s, or about 4 percent of our G.D.P. over the same period — more than we currently spend on defense. This, too, made asset owners richer.

The Trump years supercharged another bull market that would be supercharged again, paradoxically, by the Covid pandemic. When the Fed and Congress stepped in to prop up markets and assist the economy, they fueled yet another boom in asset prices — this time with more everyday Americans trying to get a piece of it, investing in everything from Tesla options to JPEGs of apes. The retail investors have seen winners and losers among them, while the billionaire class as a whole has absolutely flourished. Over the last five years, Jeff Bezos’ fortune has more than doubled; Elon Musk’s, fueled in part by retail investor exuberance, has grown by a factor of 20.

In fairness, 2019 was something of a trough year for Bezos, what with a $38 billion divorce settlement. That he’s managed to not only recoup that but significantly increase his pre-divorce net worth since is staggering.

But the more mundane cases are really more interesting than the famous ones.

I asked Dolan what her profile is of a billionaire whom she’d never find. She told me it’s someone who quietly sold a stake in a business for, say, $250 million in the ’90s, then invested it well. Today, a guy like that could use his wealth to do whatever he wanted: buy truckloads of Nazi memorabilia, try to persuade your mayor to privatize the city’s sewers or maybe both, and you’d be none the wiser. And in fact, he wouldn’t even have had to be all that smart with his money. If he parked $250 million in an S.&P. tracking index fund in 1992 and left it alone, he’d be worth more than $4 billion today. (Dolan cautioned that no one would be quite crazy enough to put all his money in the market; nevertheless.) He would have slipped through the billion-dollar barrier like an Olympic diver. And now he’s just a guy with an insane Schwab account, some interesting ideas about sewage treatment and the world’s largest collection of authentic Totenkopf rings.

The sneering tone notwithstanding, this re-emphasizes the key variable: having a large pile of money that can be left alone to grow into a massive pile of money while still enjoying a nice lifestyle. The quarter million in 1992 dollars would be worth $571 million in today’s money. But thirty years of compounded returns increases that seven-fold.

And, of course, the larger the pile the easier it is to increase it. If you have a few billion laying around, you can invest a few million in a couple hundred startups and, if even one of them makes it big, you come out ahead.

Here’s the top twenty on the Bloomberg billionaires list as of this writing:

Rather obviously, it’s dominated by people who call the United States home, including South Africa-born Musk. And almost all of the “new” money is in the technology sector (although, in fairness, Amazon started as, and in some ways still is, a retail company).

That Musk’s estimated net wealth has doubled this year—indeed, it has increased almost as much as Bezos’ total net worth—just boggles the mind.

That the three Waltons, all of whom inherited their money, are worth a combined $340 billion is noteworthy. Two others make the list at #40 (Lukas, at $39.6B) and #120 (Christy at a measly $18B).

Circling back to the subject of Steven’s post, it’s actually remarkable how few of these folks are front-and-center in American politics. Musk seems to have emerged in that role only in the closing weeks of the campaign. Charles Koch, the remaining living Koch brother, is ranked #22 ($65.8B) and has obviously been heavily influential for decades. But I recognize far more of them from their investments in professional sports than I do politics.

*There are multiple variants but this was the only one I could find a decent transcription of. The one I was looking for the punchline, “I had to host the Oscars to get that house — a black dentist in my neighborhood would have to invent teeth.”

I’ve been trying to popularize the idea that property rights diminish as wealth is accumulated because the nexus between the creation of wealth and the reward diminishes.

For example- If you plant vines and tend them and harvest them and press them into wine, well, most people’s moral intuition is that the wine is legitimately yours. You created it and can claim property rights over it.

But as your business expands and you hire people to make the wine, and then expand and gain investors in stock sales, the nexus between the creation of the wealth diminishes.

At some point your wealth isn’t from making wine, its from stock value and the power of money to make money.

At this point it is rightful to question if you actually have a legitimate claim over the wealth being generated.

And at some point your right to claim the wealth diminishes to zero.

You know, I kind of discount “it’s a global phenomenon” when most of the names on the list are Americans, and the rest can just buy stock in what’s now known as The Magnificent Seven (all us own stocks: Apple, Google, Microsoft, NVidia, Meta, Amazon, Tesla), which are all US-based companies. As you cite Piketty pointing out.

So yeah, I think US policy has a very significant impact.

Eh, I dunno, James. It would be laughable to claim Republican policy=global policy. But it would be equally laughable to claim that US soft power is non-existent.

Neoliberalism has been something of a global consensus for a few decades. China, the obvious counter-example, moved toward liberalization without going all the way.

@Chip Daniels:

This is a good idea to popularize.

I would point to different aspects of property rights, but overall, I think your point is pretty solid.

Many of the names on the list are “quiet” politically, which I appreciate. However, they still have an enormous ability to shape the choices I have as a citizen – and I’m not poor.

I have harped before on AI. It is designed and organized not to serve your or my needs, but the needs of the billionaire (or moneyed interest if you prefer) that funded it. That seems proper in a capitalist society, and yet it precludes me from having an assistant that actually helps me, as opposed to trying to troll me into clicks and rage-induced spirals through trollish content.

That’s one example of the phenomenon.

Basically in life once you have a set amount of capital you can make tons of money just by existing. You no longer have to be creative or even proactive. You just need to know how the wall street “game” works.

Speaking of games I’ve seen similar happen in every single multiplayer online game that has a free market. It’s inevitable some handful of assholes will monopolize the markets and drive up prices for profit. Sometimes the asshole got there by exploiting a niche market but most of the time they got there by buying in game currency with real money. Kind of like having an inheritance in real life.

The uber rich in the USA are by this point just running up their high scores. Unfortunately that leaves the rest of us to fight over smaller and smaller cuts of the wealth in this country.

What’s almost amusing is that Elon is literally doing everything that the right claims Soros does…

@Jay L Gischer:

They’re not quiet, they’re just not speaking to you.

Let’s not forget another source of wealth: the manipulation (legally, of course) of the tax system to increase your net worth outside of the actual business growth of the wealth. The archetypal case is that of Mitt Romney putting under valued assets into his Roth IRA and growing legally and tax-free to $100M from there. Manipulation of wealth is an international game for the wealthy. Technically, I guess such techniques are available to us scum of the earth but not realistically. And we don’t have the funds to urge insertion of tax law into the code for the benefit of a few.

Most of them founded successful companies that went public and those companies continued or increased that success, thereby increasing the value of those companies. Most of that wealth is tied to the stock value of the companies they founded and increases or decreases with the company’s fortunes. That’s how Musk’s wealth has increased so substantially lately – it’s almost entirely due to the increase in the value of the companies he founded.

Most of the rest are like Forrest Gump or Warren Buffet – made good early investments in some of those same companies or the markets generally and benefitted from their success as values grew.

IOW, few get billions in wealth from having a high income. The whole discussion about 70% (or whatever) income tax rates is a red herring because wealth generated from the increasing value of a company or stock portfolio isn’t income until it’s cashed out in the same way that your 401k or IRA is not income until cashed out. It’s the same concept of wealth building that normal people use only on a much bigger scale.

Most of them are in the US because we are better than anyone else at fostering the kind of environment that allows Walmart, Google, Amazon, Microsoft, Tesla, etc. to be founded, grow, and succeed. To the extent people think billionaires are a problem, it’s not clear how to prevent billionaires without some kind of wealth tax (tried in Europe and turned out to be a dumb/bad idea) or changing regulations/market conditions such that successful companies can’t be formed or can’t grow which is easier said than done and probably also a dumb idea.

@Matt:

Mark Cuban, a billionaire himself, has proposed that one could buy out the entire coal industry (buy all coal plants at a profit to the owners, full pay to all current employees until retirement, transition time for customers) for about $36 billion. Think about that for a moment. Any of the top ten people on the list above could remove a key driver of climate change to the benefit of the whole world and still be left with $100B to buy professional sports teams, mega-yachts, and congressmen.

But instead of solving problems, they’re “running up the score.” Or in Musk’s case, spending his money to sell the masses on government “living within its means” for the sake of tax cuts. I’m a proud capitalist, but someone needs to explain to me how this isn’t f’ed up.

@Andy:

Could you share more specifically by what criteria wealth taxes tried in Europe turned out to be dumb/bad? Were the taxes cleverly avoided? Was the additional revenue squandered? Were there adverse impacts to the broad economy?

I, for one, see billionaires – or more precisely massive and growing wealth inequality – as a societal problem, so it would help to better understand what hasn’t worked when trying to improve it.

Among other things, we took the chains (that were imposed during the Great Depression) off the finance industry. Anything can be securatized now, and the price run up astronomically by people playing with piles of paper, completely disconnected from any sort of underlying value. One of Cain’s Laws™ says: Any situation where it is easier to become wealthy by manipulating financial instruments than by producing the underlying goods and services will end very badly.

@Andy:

True enough. And given that reality, the argument for raising tax levels for high-income earners, particularly for the segment for whom said income is a miniscule portion of significantly larger wealth, should be reexamined. Maybe taxes only need to be high enough to stimulate transfer of capital from the accumulation pile back into the spent resources pile.

These guys aren’t billionaires because of tax strategies or finance. Almost everyone on that list is there because they collect data on people, offer scaled-up means to manage and analyze this data, or use that data to sell consumer goods to people. The last stage of a capitalist center is always abstraction. In this case, it’s globalized.

It’s telling that the idea of the public company with a CEO nominally behold to shareholders is probably becoming a relic. Privately-held companies are more popular for investors now. They want the black box. It’s like the last stage of public accountability is being shed. In maybe fifty years, these lists might not have any real names on them.

But as your business expands and you hire people to make the wine, and then expand and gain investors in stock sales, the nexus between the creation of the wealth diminishes.

At some point your wealth isn’t from making wine, its from stock value and the power of money to make money.

At this point it is rightful to question if you actually have a legitimate claim over the wealth being generated.

In the case of wine, you’re taking an inherent risk in an insanely-competitive market. Vineyards are high-end agriculture. Unless you seek outside investors, you are bearing the risk on your own, and at a certain level, you deserve the profits you get.

On your bigger point, creation is always contradictory. Medieval guilds credited a painting to a master even though his assistants might have done the grunt work. I’m not an expert, but I don’t think this confused anybody about the origins of a work. It’s modernity which made individuals into singular geniuses. Some of that makes sense. Science and art allow for actual authorship. And Hegel thought Napoleon was the world spirit in action or something. Commerce just emulated science, art, and politics, even though art in the 20th century became antagonist towards this idea.

@Modulo Myself: Arguably only Bezos, Zuckerberg, Page & Brin fit that description and they made their money by creating unique products that later were used to gather and build the data.

@Scott F.:

Lots of reasons:

– Difficulty in valuation

– High administrative/enforcement costs

– Wealth mobility (rich people and businesses moved somewhere else)

– It’s easier in some ways to avoid via tax planning/strategies

– Revenue generation never achieved promises.

The billionaire class? I read recently that Elon Musk, Larry Ellison, Jeff Bezos, Mark Zuckerberg, and Bill Gates combined have well over a trillion dollars in wealth now.

In the 2020 Citizens United case, The Roberts Court ruled that money is speech, as such there can be no limitations on spending on elections. So when it comes to spending money on elections Elon Musk has a lot more speech than anyone else in America. Elon Musk ‘donated’ over a quarter of a billion dollars to the Trump campaign, apparently it came with strings attached.

To the basic question> They (Billionaire Class) came to be through tech innovation, and just as important through significant changes in American tax law and policies that enabled these people amass great wealth. The old ‘rules’ and ‘norms’ regarding valuation based on price and earnings do not apply now. Companies may often go for years without being ‘profitable’ by a ‘normal’ standard. As long as they can attract investors a company may survive until it turns the corner and goes public, which often results in a new class of multi-millionaires and in a new class of billionaires too.

And … here we are. Republicans have turned over the keys to our government to these people.

Babylon 5 had a story line where a billionaire develops a virus that kills only telepaths. the Psi Core takes care of that matter, with extreme prejudice as is their custom.

Now, had the telepaths developed a virus that kills only billionaires…

I recall my father, a rather conservative chap in many ways.

But also an advocate of distributism and the co-operative movement.

The Common-Wealth Party may yet rise again! 🙂

That stream was also part of the European Catholic “Christian social”politics, one origin of modern Christian Democrats/Christian Socials in Germany, Italy, and France.

Which has also been seen as one of the originations of fascist political thought.

Mistakenly, imo.

Much of the “Catholic Centre” of Europe in the 1930’s ended up aligning with the fascists, but that was largely a historic accident.

And the British version was never so compromised by being aligned with European Catholic anti-liberal and anti-socialist inclinations.

That is, I think, a serious criticism of our supposedly liberal MSM. They seem reluctant to go behind the green curtain and talk about who’s paying for what. What percentage of the public do you think have any idea who, say, Miriam Adelson is? Or who owns Uline?

@Michael Cain:

A security is a piece of paper worth about a tenth of a penny a copy. The value is that a security represents, ultimately, a legal claim to (contra you) underlying cash flows (or intermediately, assets). No one can or does create value or increase value by “playing with pieces of paper.” That is a simplistic, arrant nonsense really, comment.

There are arguments for and against securitization. But your comment indicates that your understanding of finance approaches zero.

But I have a broader question to James and the entire thread. Why do you care? You could simply confiscate the entire net worth of all these billionaires and run the government for a few hours. What have you accomplished other than to satisfy your envious personality flaws? We do not have a taxing problem. Unless these people adversely affect public policy, and you point out most of these people are politically silent, we do not have a billionaire problem. We have a spending problem. Which is a politician problem; and since politicians react to voters and voters vote these people in over and over because they perceive a free lunch….we have a citizen/voter problem.

Oh wow. This is really cool. Not only in being an inspiration and being correct about my hunch.

I was also a huge fan of the book of lists. I had a copy from the 80’s that I would read constantly. I suspect it laid the foundation for how I think/express ideas. Between ADHD and some form of expressive learning disability I organize things in lists and then flesh them out. Interesting.

@Andy:

I am genuinely curious if you think:

1. The U.S. would not have successful major companies if we had a high income tax/wealth tax; and

2. Do you think Billionaires as opposed to the ordinary very rich are inherently destabilizing?

I’m interested and genuinely curious because, admittedly, I’d like to make my argument better.

One argument I hear from my conservative friends is that we can’t have a high income tax rate or a wealth tax is because investors are putting their money at risk and they could lose everything.

Setting aside that is pure gambling. I think it is also propaganda. What’s the difference between an investor who puts his wealth on the line to make money versus a coal miner who puts his life on the line to make money?

To me it’s the exact same thing except the investor is likely to make more money even if he loses it all, where as the coal miner is just dead.

I get there may be gains or losses depending on when that investor takes his money out. But why can’t we tell the investors to realize, even if it’s just on paper, their gains and losses each year and then get taxed on that? It would probably force a lot of them to sell to cover the taxes, but at a certain amount of wealth it won’t matter.

I think that sort of tax set up might get some of these companies to push more of their profits towards their workers. Which I suspect would stabilize a lot of things/problems in this country. Without destroying the environment that allows such companies to thrive.

The people on that list are flesh and blood and have limited terms on this earth. I wonder if they will be able to establish a long term hereditary class of elite billionaire scions. So far, in the USA we haven’t had a lot of hereditary elites. I’m not aware of any descendants of JP Morgan or Rockefeller that are exceptionally powerful. The Kennedy and Bush clans appear to be in sunset mode. Donald Trump, Jr. and Eric don’t give off vibes of establishing generational power.

@Slugger: how many of them are even trying to?

@Slugger:

Ever hear of the WASPs? They ran the government, the banks, and the media for a long time. When you see guys like Mark Andreessen talking about reversing the New Deal or whatever, they’re talking about reversing FDR’s class-traitorism.

@Beth:

The main problem with the wealth tax is that it requires constant vigilance at lower pay. America is a country where people think a loophole which allows SUVs to play around with mileage standards is more natural than the science behind climate change. You would need a cultural revolution to get people who are good with screwing around with numbers on balance sheets to end up in the IRS rather than on the other side.

@Beth:

I’m reminded of this country in the 50s and 60s that had a rather high income and corporate tax rate, yet it led the world in manufacturing and innovation in cars, aerospace, computers, electronics, and other areas. It also managed to keep up a large military force.

What was it called? Oh, yes, the United States of America.

I’m also reminded of a so-so novel called “Buying Time” by Joe Haldeman, of “The Forever War” fame.

The gist of the novel is a medical technique that restores perfect health and extends life, ten years at a time. It’s controlled by a foundation, and they keep their secrets tight. It’s sold to anyone for a price: everything you own, so long as it’s at least one million pounds (one presumes Sterling).

The idea is to stop wealth accumulation. Nice theory. In practice, people game the system, hide assets, borrow from each other, etc. and keep on getting richer over time, despite giving up “all” their wealth every decade.

So, what @Modulo Myself said.

@Andy, @Modulo Myself, & @Kathy:

I’m not a huge fan of the “it’s too easy for the super-wealthy to avoid the taxes and game the system” rationale for surrendering in advance.

The unhealthy shift toward oligarchic power that Steven fears seems evident. I would argue that smart people being convinced that it would be dumb/bad to even try to mitigate the situation is evidence the shift is already established.

Among people with real wealth, none of it came from their own labor. I’m at the high end of how wealthy one can get just from being paid a salary and investing it wisely, and I’m not a 1%er, much less a billionaire.

Extreme wealth comes from a combination of luck, inspiration, and increasing returns to scale. Luck can be accident of birth, happening to win the semi-random market competition, or timing. Inspiration, while generally cited as the sole factor by conservatives, is usually a relatively small contributor. Bill Gates and Warren Buffet were not significantly more inspired than thousands of non-billionaires. Returns to scale, on the other hand, are universal — money makes more money, and larger amounts of money generate higher rates of return than smaller amounts. Once you are rich, you cannot help but become ultra-rich, barring extreme ineptness. (Trump’s failure to become ultra-rich is telling.)

@Scott F.:

I agree. But it won’t be easy to tame the oligarchs and keep them tame.

@Scott F.: Re: the Mark Cuban story….

I understand passive investors gaining wealth, hell – I am one since retiring at age 53 in 2018.

The folks still “working” Musk, et. al., however, value their life energy so little that they are willing to spend their limited time on earth accumulating money that they will never be able to use. And apparently, CEO is such an easy job that Musk can do it for 3 or 4 companies simultaneously while presiding over the country as the de-facto president-elect.

This is a pathology I’ll never understand. At some point, you are trading something you have less and less of (your time) for something you have tons of (money).

@DrDaveT: There’s an aspect to accumulating money that is missing from your list – psychopathy.

It is nearly impossible to be a billionaire without having a breathtaking disregard for the plight and fortunes of the people around you who enabled it and actually earned it.

There are a few examples of exceptions – Taylor Swift comes to mind – but they are rare.

One Utopian idea of mine is a law that would require that no individual be permitted to hold in his or her own name business assets valued at more than $ 1 billion. Any assets valued at more than that amount would have to be put into a trust, from which the individual could draw a set amount of income. Increases in asset value would benefit the trust, not the individual.

@Beth:

This is something where the details matter quite a bit, but in general, I’ve long advocated for higher income taxes, a less complicated tax system (to avoid gaming and to reduce compliance costs), and implementing something like a VAT. I think the evidence is strong that wealth taxes are, at best, suboptimal.

If I were King and could make the tax system the way I want, I would eliminate most business taxes, greatly reduce the complexity of the tax system to reduce gaming and tax compliance costs (tax compliance costs are currently about 2% of GDP, or over half a trillion annually), treat realized capital gains as regular income, adjust income rates to make up for the loss of business tax revenue, and institute a progressive VAT, which has been much more successful than the various experiments with wealth taxes.

No, I don’t see much evidence that billionaires are inherently destabilizing. I read a lot of people asserting it as a fact, but the evidence always seems to boil down to a lot of handwaving and focusing on an arbitrary “billion” number and “billionaire” label. A much bigger problem, IMO, is powerful interest groups and over-consolidation in many industries that are effectively the biggest players in influencing Congress and our political system.

Profits are different from a company’s paper value. Billionaires do not get their wealth from profits sitting in a bank account—their wealth is the primarily driven by the value of the companies they own. I have no problem with providing incentives to drive more profits to a company’s workforce, but that is a different thing from the value-derived wealth that makes billionaires into billionaires.

@Scott F.:

Avoidance and gaming the system aren’t the only reasons I listed. There are well-documented reasons that Europe mostly ended wealth taxes in favor of consumption taxes (e.g., VATs). If they missed something and wealth taxes are actually great, then we really need some evidence.

@Kathy:

That was a time when the US had no competition because the rest of the world’s industrial powers were destroyed (except maybe the USSR, which was not a capitalist system). The high tax rates were instituted to pay for that war, and it was America’s unique position at that time that allowed all kinds of policies to work that won’t and wouldn’t be possible in today’s globalized environment.

The 50’s and 60’s were also a time of high tariffs and extremely low immigration, for example. What do you think of the argument that we can have high tariffs and low immigration again because we did it in the 50’s when things were so great? Because that’s the argument Trump and his supporters are making, and it’s just as flawed as any other version of the “we did it in the 50’s, so we can do it today” argument.

It’s actually a steeper climb to billionaire status than that. Considering taxes and expenses, that $100 million a year income doesn’t get someone to $1 billion in 10 years. Hardly.

But, investment and stock options and stock growth does. How much of Musk’s $400 billionaire status is on paper?

And that brings us to this: the monopolization of wealth leads to further aggregation of wealth by an order of magnitude. There’s no catching up, the inequity gap only widens. And with it grows the potential and opportunity for corrupting our democracy and upending equal access to policy making.

There is a solution, if we believe in and desire to maintain our liberal democracy. That solution is regulation; limiting monopolistic practices, taxing the wealthy on a sliding scale, including estate taxes etc. That kind of regulation is precisely why a component of uber-wealthy (including sub-billionaires) have backed “libertarian activism” and throughly taken over the Republican Party.

Unfettered access to wealth-making by the wealthy is the prime GOP plank now. All that other stuff, gun ownership, pro-life, anti-woke, transgender bathrooms etc., is mere strategy to get the votes of the un-wealthy.

Without the votes of the “hoi polloi” the wealthy simply do not have the numbers to vote in the policies that make their lives a bowl of gold encrusted cherries. The wealthy have bought a major political party, major media outlets, and political strategists in order to fulfill plan.

Create conflict, discord, outrage in the common ranks over gender pronouns, refugees, transgender story hours, then divide and conquer. It’s working. It has succeeded to the point that previous societal taboos like neo-nazism, bigotry, and misogyny are out in the open and even touted.

One additional part of the solution: campaign finance reform. But with the magnitude of wealth arrayed against reform, that is another uphill battle.

We have a decision to make: capitulate to this remaking of a society born of hard fought battles, or to fight like hell.

@Andy: I can understand why the second half of your sentence is true, because it stifles innovation, but why is the first half true? Why is a wealth tax a bad/dumb idea?

ETA: I see that Scott asked this question before me.

@Monala:

I answered here.

Europe tried wealth taxes for a very long time and has mostly abandoned them for those reasons.

@Andy:

I see this assertion, that the 50s worked because we had no competition, but is it proven? By proven I mean is this the accepted consensus among economists?

I mean, what is the connection between “being able to have high taxation” and say, “Japan not being able to export cars to America”.

Like, what would happen if we did raise taxes? Would somehow the availability of cheap Chinese imports no longer exist?

I honestly curious about the mechanism that links taxes to foreign trade.

The reason for the increase in billionaire is quite straight forward. In the Gilded Age, tycoons had a market of few tens of millions of people. Today, they have a market of billions. Microsoft claims to have 1.5 billion users. That’s … what, 100 times what Henry Ford ever had? More?

I seem to have born without the gene for wealth envy, though, because I really don’t care if other people get very rich. Global poverty has been falling. Incomes have been rising. Unemployment is at record lows. Jeff Bezos’ wealth does not make me poor. On the contrary, it gives me ways to increase my buying power.

The intersection of wealth and politics is concerning but I would say it’s just more open and blatant now. It wasn’t like FDR hobnobbed in the slums.

@Chip Daniels:

I think it depends on exactly what tax you’re talking about.

For instance, effective (not marginal) corporate tax rates in the 1950’s were 40-45% compared to around 25% today (depending on the state the corporation is in). Even at 25%, the US has one of the higher corporate tax rates of comparable countries – the global and OECD average is about 23%. Raising that up by a further 20% would make the US a massive outlier, make US businesses much less competitive compared to foreign firms, and give them a strong incentive to leave the US or take profits overseas. There aren’t many (if any) economists who would say that effective corporate tax rates of 40-45% wouldn’t have severe negative effects. The only reason it worked in the 50’s is because the US was a massive net exporter thanks to being the dominant world economy, and we had highly protectionist policies (like tariffs) on foreign goods.