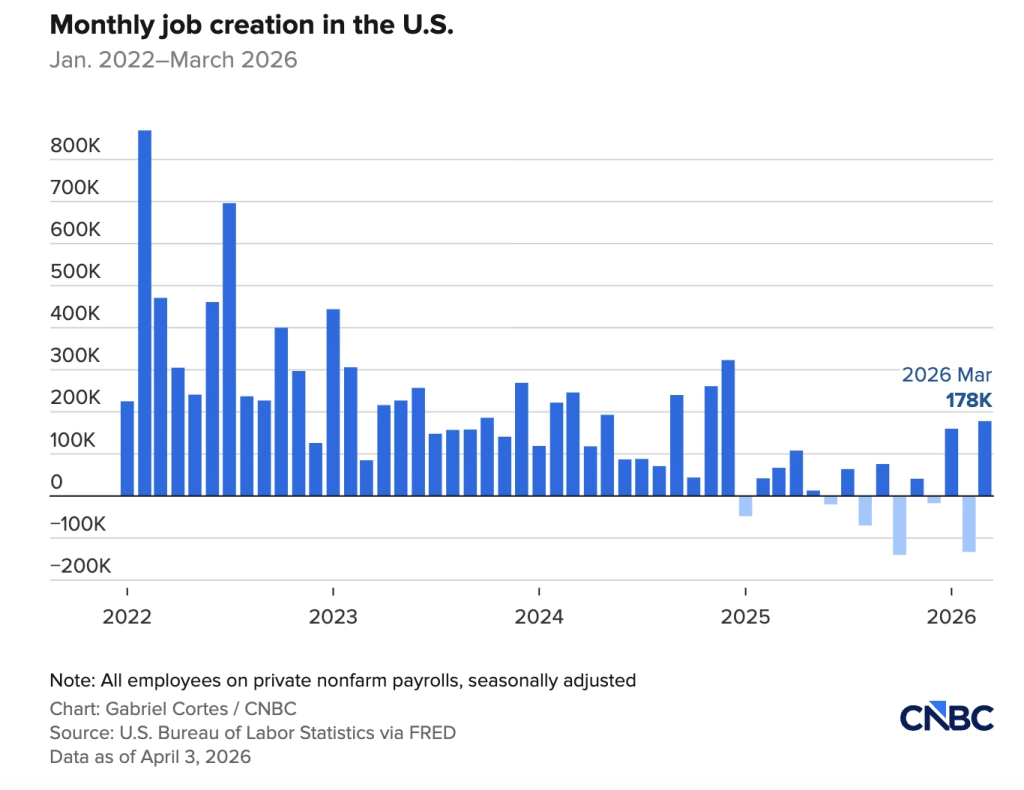

First, some modest good news via CNN: The US economy added a higher-than-expected 178,000 jobs last month.

The US economy added 178,000 jobs in March, a signal that businesses were moving forward with hiring plans before the war with Iran escalated.

The unemployment rate eased to 4.3% from 4.4%, according to new data released Friday by the Bureau of Labor Statistics.

Economists expected a net gain of 60,000 jobs, a rebound after a surprising swing negative in February when 133,000 jobs were lost.

All well and good, but let’s put that in perspective (via CNBC):

More from the CNBC link:

“The bottom line is March was somewhat encouraging, but it’s been a rocky year for the labor market with almost no hiring since last April,” said Heather Long, chief economist at Navy Federal Credit Union. “The March data will keep the Federal Reserve on hold, but no one is declaring victory yet. It’s likely to be a tough spring for job seekers.”

As has been the case, health care was responsible for much of the growth, with the sector adding 76,000 jobs. A strike at health-care provider Kaiser Permanente in February hit the sector. The BLS said ambulatory health care services rose by 54,000, with 35,000 coming from the strike workers returning.

Construction saw an increase of 26,000, while transportation and warehousing posted a gain of 21,000.

On the downside, the federal government saw a loss of 18,000, while financial activities lost 15,000.

[…]

Wages also rose less than expected, with average hourly earnings up just 0.2% for the month and 3.5% from a year ago. Economists had expected respective readings of 0.3% and 3.7%. The annual increase was the lowest since May 2021. Hours worked declined 34.2, down one-tenth from February.

And then there’s this:

Via CNBC: Brent oil spot price for actual cargo soars to $141, highest level since 2008 financial crisis.

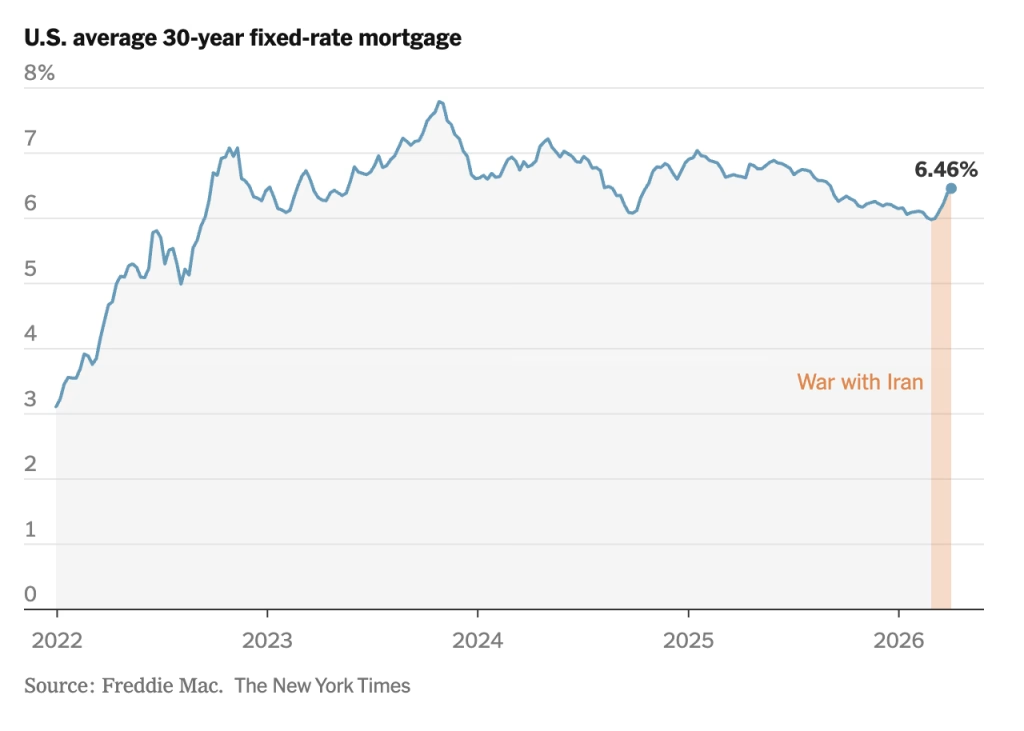

Via the NYT: Mortgage Rates Climb for 5th Week as Iran War Weighs on U.S. Housing Market.